Unabsorbed Business Loss Carried Forward Malaysia Lhdn

Budget 2019 The Proposed Tax Changes That The Business Must Know Cheng Co

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2019 2 Pdf

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2019 2 Pdf

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2019 2 Pdf

What Is An Investment Holding Company And When Is It Useful Propertyguru Malaysia

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2019 2 Pdf

On unutilised losses and allowances currently there is no time limit for carrying forward of unutilised losses and allowances.

Unabsorbed business loss carried forward malaysia lhdn. Finance minister lim guan eng tables budget 2019 at parliament in kuala lumpur november 2 2018 picture by shafwan zaidon. Any unutilised losses can be carried forward indefinitely to be utilised against income from any business source. This is to minimise the revenue loss of the government in the sense that a business that continues to be loss making is unrealistic. Kuala lumpur nov 2 business entities are allowed to carry forward unabsorbed losses and unutilised capital allowances in a year of assessment for a maximum period of seven years of assessment said minister of finance lim guan eng.

Utilisation of capital allowance is also restricted to income from the same underlying business source. The new amendments will be effective year of assessment 2019 where the unabsorbed business tax losses and unutilised capital allowance will only be allowed to be carried forward consecutively for seven years. Effective from ya 2019 the time limit is 7 yas. Business entities are allowed to carry forward unabsorbed losses and unutilised capital allowances in a year of assessment for a maximum period of seven years of assessment said minister of.

The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business income of the target company. Utilisation of carried forward losses is restricted to income from business sources only. It is proposed that a time limit will be imposed as follows losses allowances proposal 1. Unutilised losses accumulated as at ya 2018 can be utilised for utilised for 7 consecutive yas and will be disregarded in ya 2026.

Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward indefinitely. Unabsorbed losses not to be carried forward to post pioneer period. Tax exemption of statutory income for 10 years. Unutilised business losses to be carried forward for a maximum of 7 consecutive 2.

Current year adjusted loss rm 300 000 unabsorbed business losses b f rm 600 000. Approval of pioneer status by a company producing a product or participating in an activity of national and strategic importance to malaysia. Any unutilised losses can be carried forward for a maximum period of 7 consecutive yas to be utilised against income from any business source. Unabsorbed capital allowances not to be carried forward to post pioneer period.

In ya 2019 xyz has unabsorbed business losses c f of rm600 000 from ya 2018. For companies in a loss making non tax paying position.

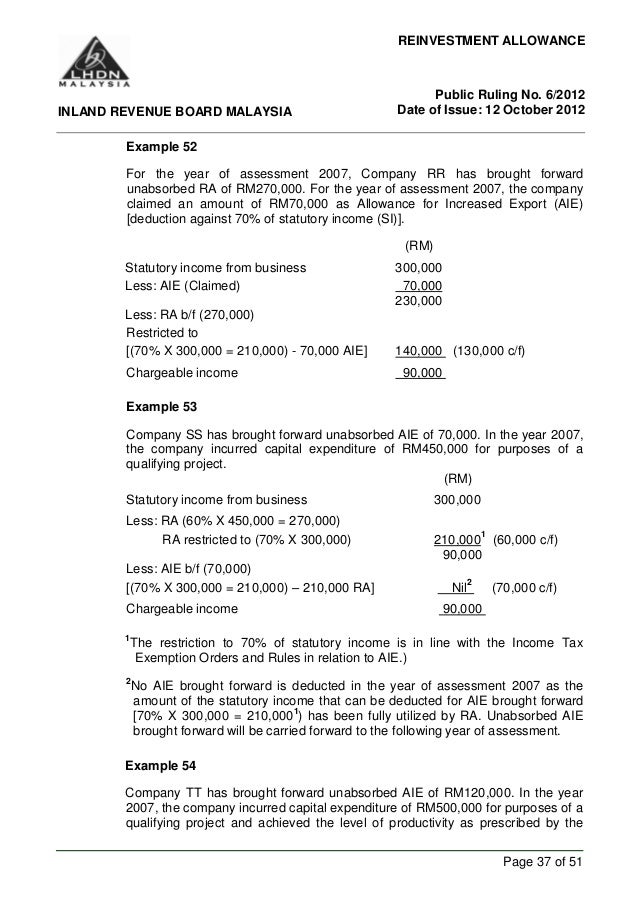

Pioneer Status Investment Tax Allowance And Reinvestment Allowance Acca Global

2

Http Www Hasil Gov My Pdf Pdfam Samplerf Guidebook C2015 2 Pdf

2

Http Lampiran1 Hasil Gov My Pdf Pdfam Samplerf Guidebook C2018 2 Pdf

Chapter 7 Capital Allowances Students

Form B Lembaga Hasil Dalam Negeri

Explanatory Notes Lembaga Hasil Dalam Negeri

Http Www Hasil Gov My Pdf Pdfam Pr 11 2013 Pdf

No 2 Bill 2012 Malaysian Institute Of Accountants

Http Lampiran1 Hasil Gov My Pdf Pdfam Pr 05 2018 Pdf

Reinvestment Allowance 2012 Inland Revenue Board Malaysia

2